Week of June 26, 2026

The Week at a Glance:

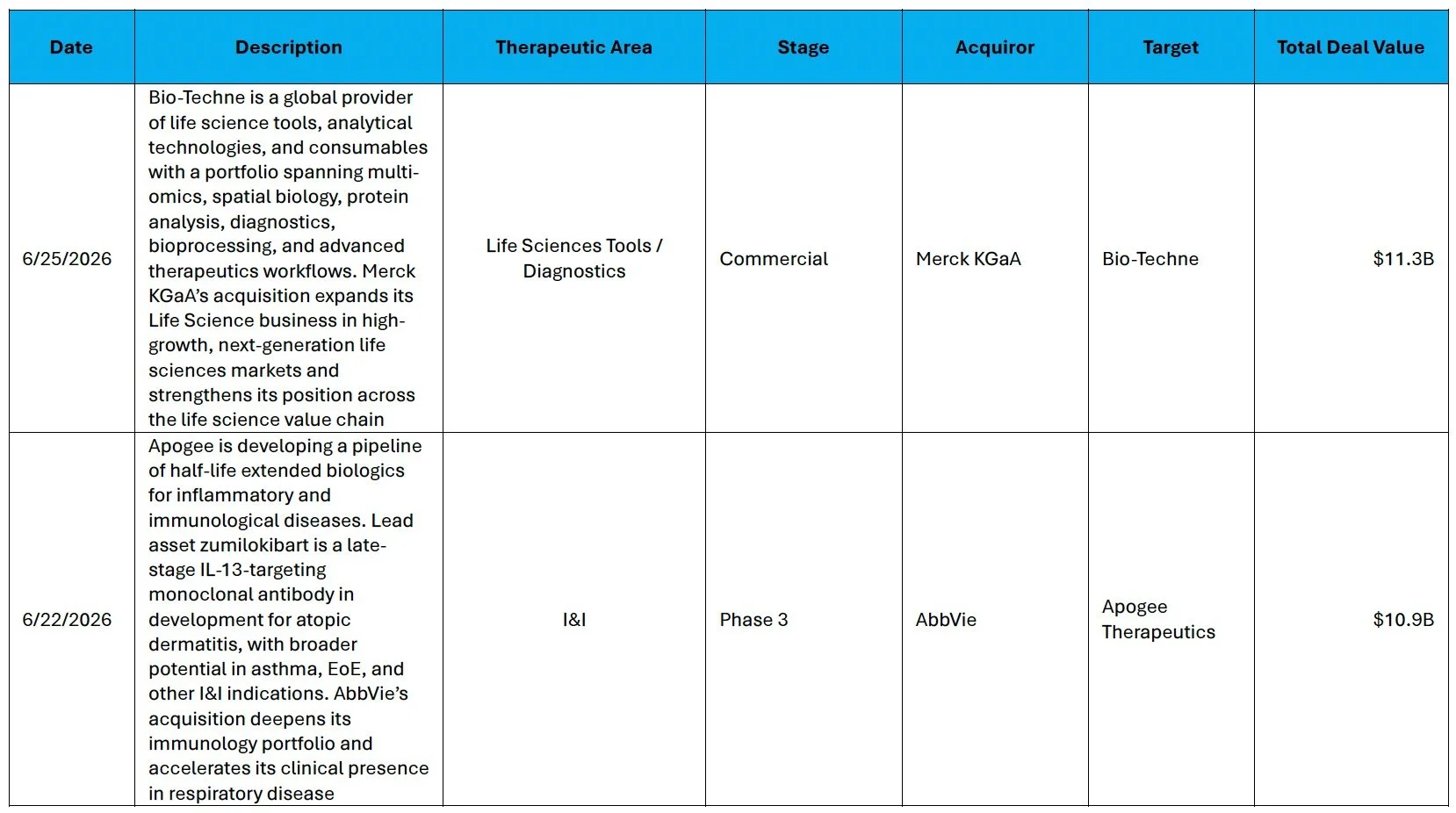

Biotech M&A Continues at a Blistering Pace: Merck KGaA announced its $11.3B acquisition of Bio-Techne, its largest deal in a decade, while AbbVie acquired Phase 3 I&I company Apogee for $10.9B

Psychedelics Show Promise: Definium reported positive Phase 3 MDD data for its serotonergic psychedelic, meeting the primary and key secondary endpoints, and raised $805M following the readout

Potential FDA Leadership Change: Former FDA oncology chief Richard Pazdur is reportedly being considered for a senior leadership role at the agency

Markets Overview

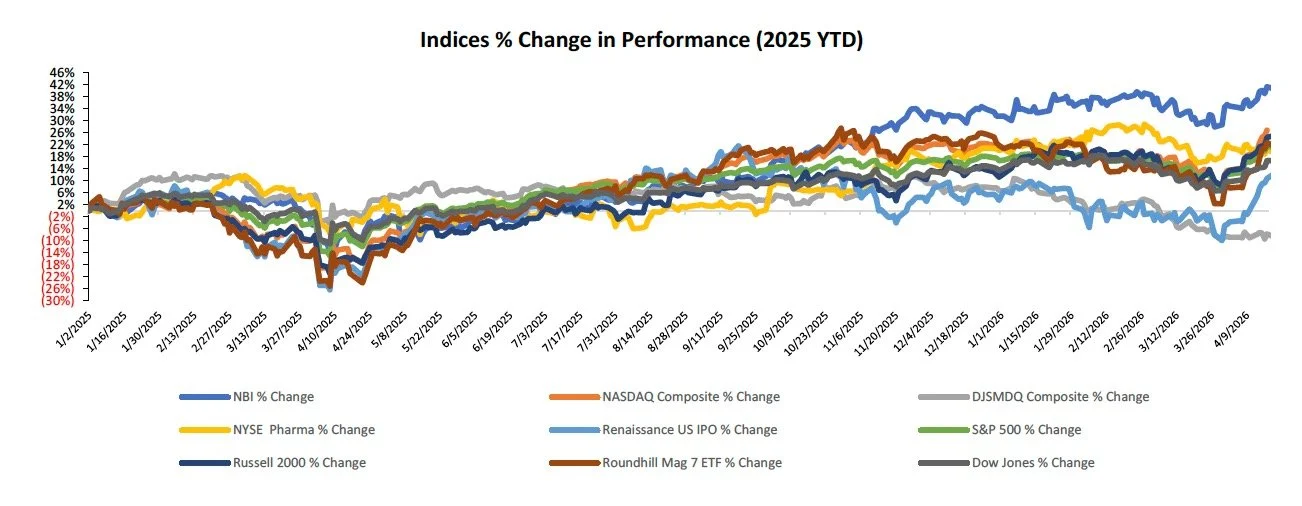

Biotech markets meaningfully outperformed broader indices as continued M&A momentum and positive clinical data further bolstered investor confidence

The Dow was up 0.6%, while the S&P 500 and Nasdaq were down 2.0% and 4.6%, respectively, last week

Weak after-market performance for SpaceX following its IPO prompted a broader tech selloff, with the Magnificent Seven leading the decline and falling 5.5% last week

The NYSE Pharma and NBI were up 9.3% and 7.6%, respectively, last week

Notable changes in share price:

Definium (NASDAQ: DFTX): Shares rose 83.6% after the Company reported positive topline results from its Phase 3 in major depressive disorder, where DT120 ODT, a serotonergic psychedelic, met all primary and secondary endpoints

Sources: Pitchbook, Biomedtracker, and CapIQ

Equity Markets

IPO

No IPOs priced or S-1s were filed last week

IPOs priced in 2025 and 2026 have generated a median and average return of 38.7% and 31.3% YTD, respectively

After-Market Performance by Stage

Clinical-stage after-market performance: 59.6% (average), 38.2% (median)

Commercial-stage after-market performance: 17.9% (average), 11.1% (median)

After-Market Performance by Sector

Biopharma: 59.6% (average), 38.2% (median)

MedTech: 12.9 (average), 9.1 (median)

Source: CapIQ

Follow On

Follow-on activity was led by Definium Therapeutics, with investor interest remaining strong across late-stage neurology

Additional financing activity was concentrated in catalyst-driven stories, including uniQure’s renewed regulatory path for AMT-130 in Huntington’s disease, MoonLake’s sonelokimab following Week 52 VELA data and a clearer BLA pathway in HS despite prior Phase 3 setbacks, and Taysha’s pivotal-stage TSHA-102 gene therapy in Rett syndrome ahead of expected 1H 2027 regulatory feedback

There were six follow-on equity offerings totaling approximately $1.6B this week

Definium Therapeutics (NASDAQ: DFTX) closed an $805M upsized public offering, including the full exercise of the underwriters’ option to purchase additional shares, to support ongoing R&D, potential commercialization preparation for DT120 ODT, if approved, and general corporate purposes. DT120 ODT is an orally disintegrating formulation of lysergide D-tartrate that recently reported positive Phase 3 results in major depressive disorder

uniQure N.V. (NASDAQ: QURE) closed a $258.4M public offering, including the full exercise of the underwriters’ option to purchase additional shares, to fund commercialization readiness and potential launch activities for AMT-130, its investigational gene therapy for Huntington’s disease, as well as a confirmatory study, broader clinical development, business development initiatives, and general corporate purposes

MoonLake Immunotherapeutics (NASDAQ: MLTX) closed a $200M upsized public offering to fund R&D, pre-commercialization and potential commercialization activities for sonelokimab, its investigational therapy for inflammatory skin and joint diseases

Taysha Gene Therapies (NASDAQ: TSHA) closed a $200M public offering to support regulatory and manufacturing development and the potential commercial launch of TSHA-102 in Rett syndrome, if approved, along with development of additional pipeline candidates

Absci Corporation (NASDAQ: ABSI) closed a $100M underwritten offering, with participation from Eli Lilly and other institutional investors, to advance ABS-201, its AI-designed anti-PRLR antibody program across androgenetic alopecia and endometriosis

Helus Pharma (NASDAQ: HELP; Cboe CA: HELP) closed a $50M underwritten offering to progress HLP003 for major depressive disorder, with Phase 3 APPROACH data expected in Q4 2026, as well as HLP004 for generalized anxiety disorder, HLP005, and general corporate purposes

Source: Biomedtracker

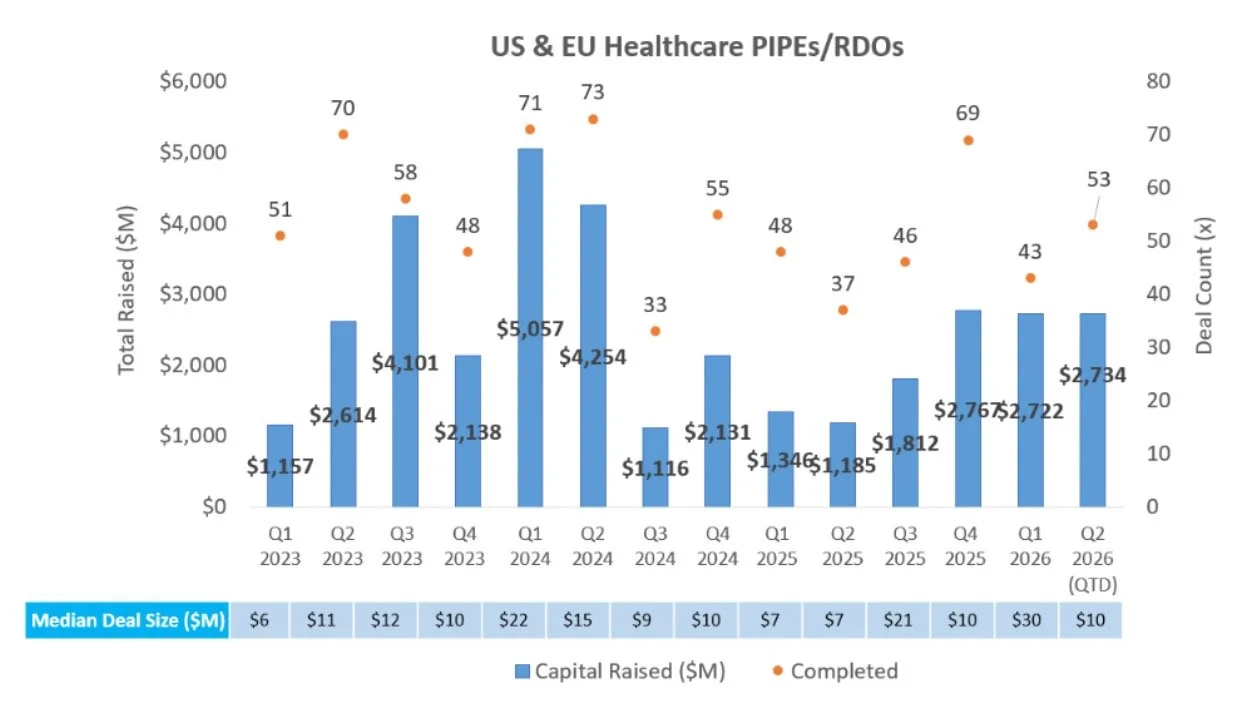

PIPE/RDO Markets:

There were three PIPEs / RDOs last week raising an aggregate of $117.6M

Remix Therapeutics raised $100M in a private placement in conjunction with its reverse merger with Passage Bio, with proceeds expected to support development of Remix’s small molecule RNA-processing therapies, including REM-422, and fund the combined company into 2028

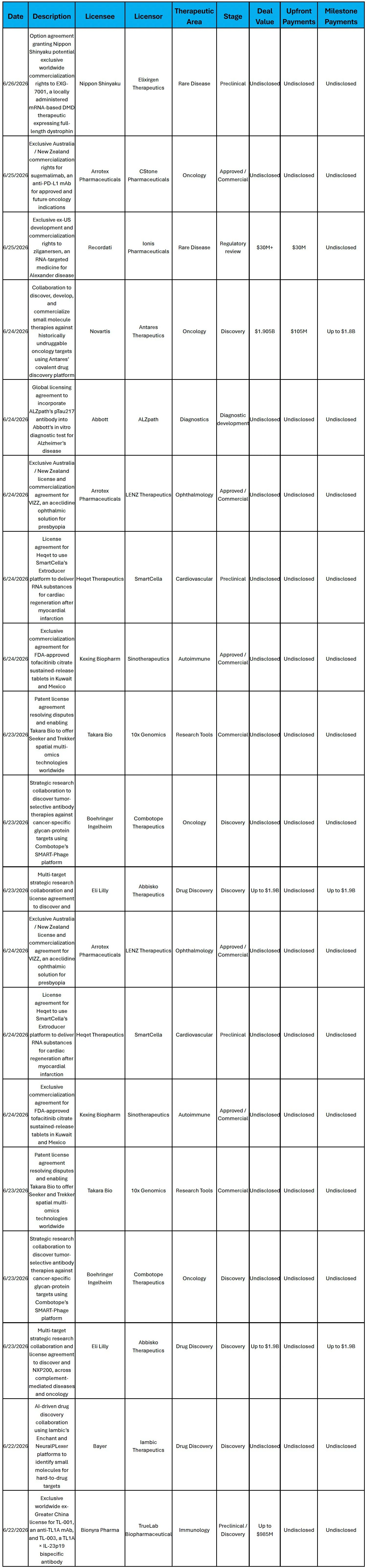

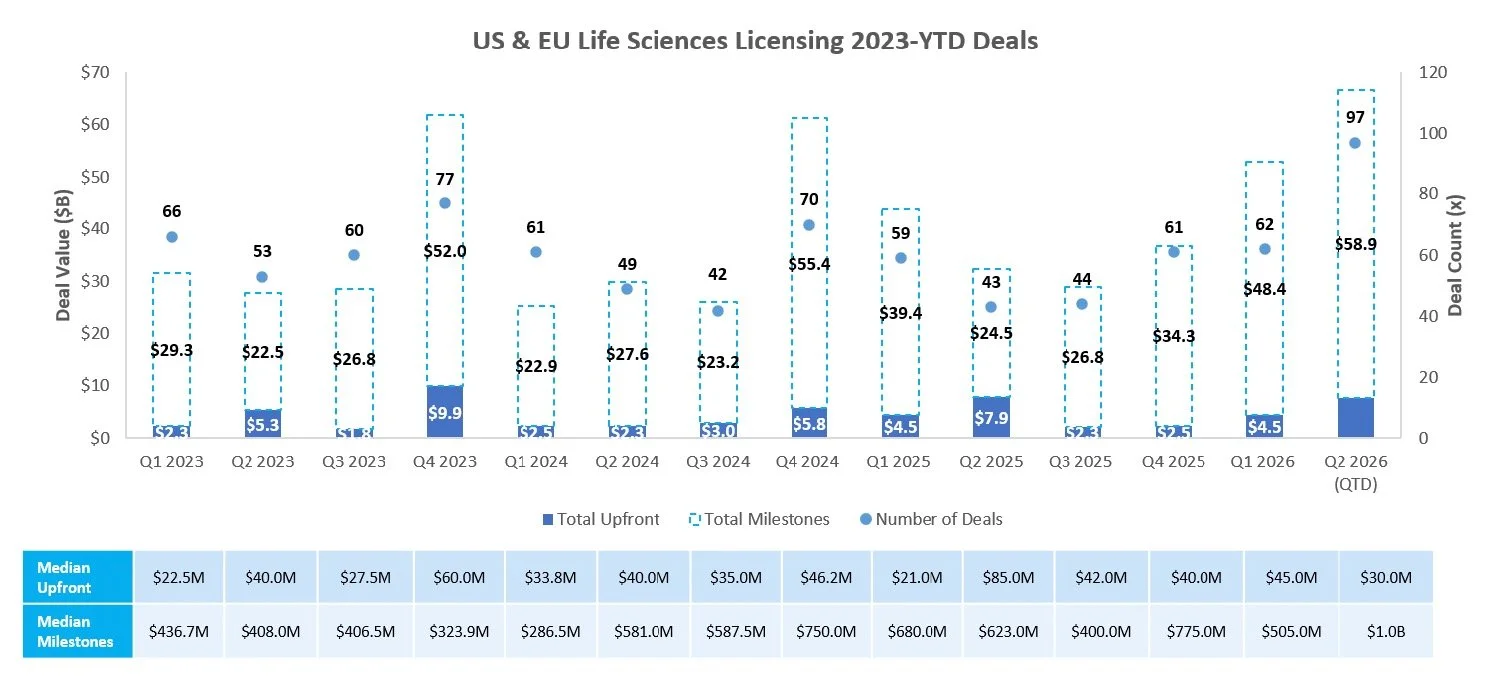

Licensing

Licensing activity was led by large AI-enabled and platform-based discovery deals, including Insilico-SK Biopharma in neuroimmune disease, Antares-Novartis in oncology, and Abbisko-Lilly across multiple targets

Additional notable activity included Nuvectis’ ex-China rights deal for two Haisco clinical-stage assets and TrueLab-Bionyra’s immunology bispecific agreement

Sources: Pitchbook, Biomedtracker, and CapIQ

Sources: Pitchbook, Biomedtracker, and CapIQ

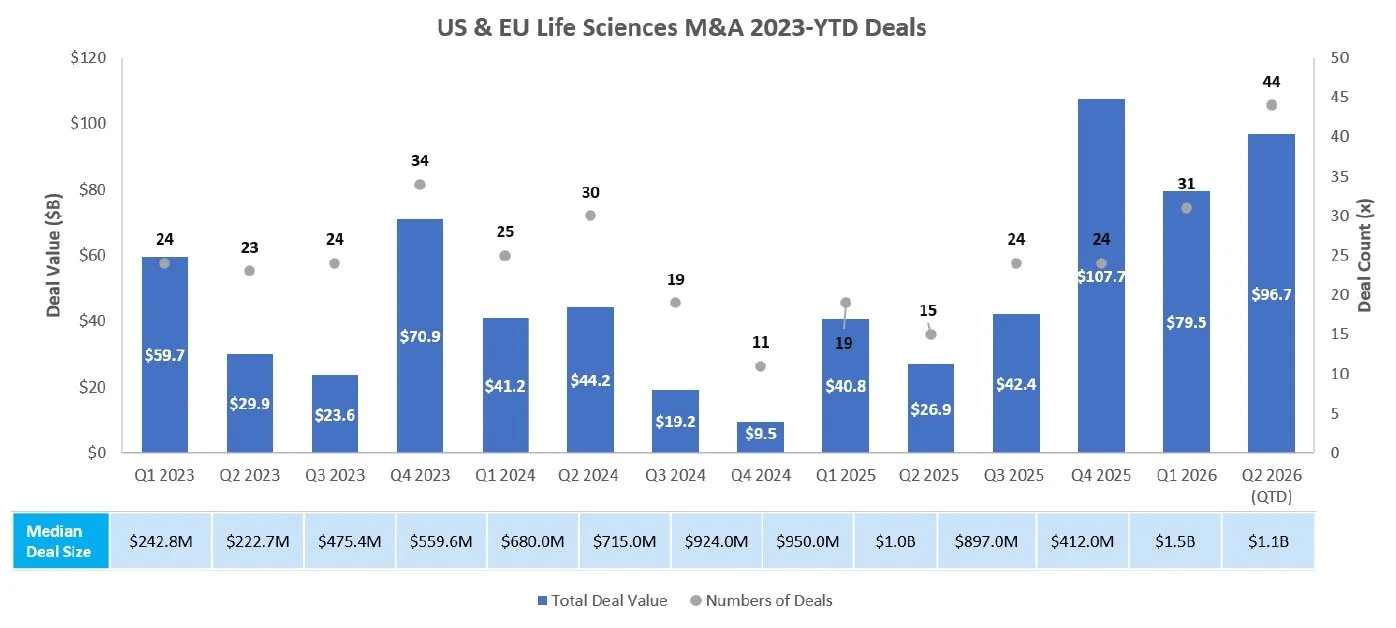

M&A

M&A activity was led by two large-cap strategic acquisitions, with Merck KGaA announcing its $11.3B acquisition of Bio-Techne to expand its life science tools, diagnostics, and analytical technologies capabilities, and AbbVie announcing its $10.9B acquisition of Apogee Therapeutics to strengthen its immunology pipeline

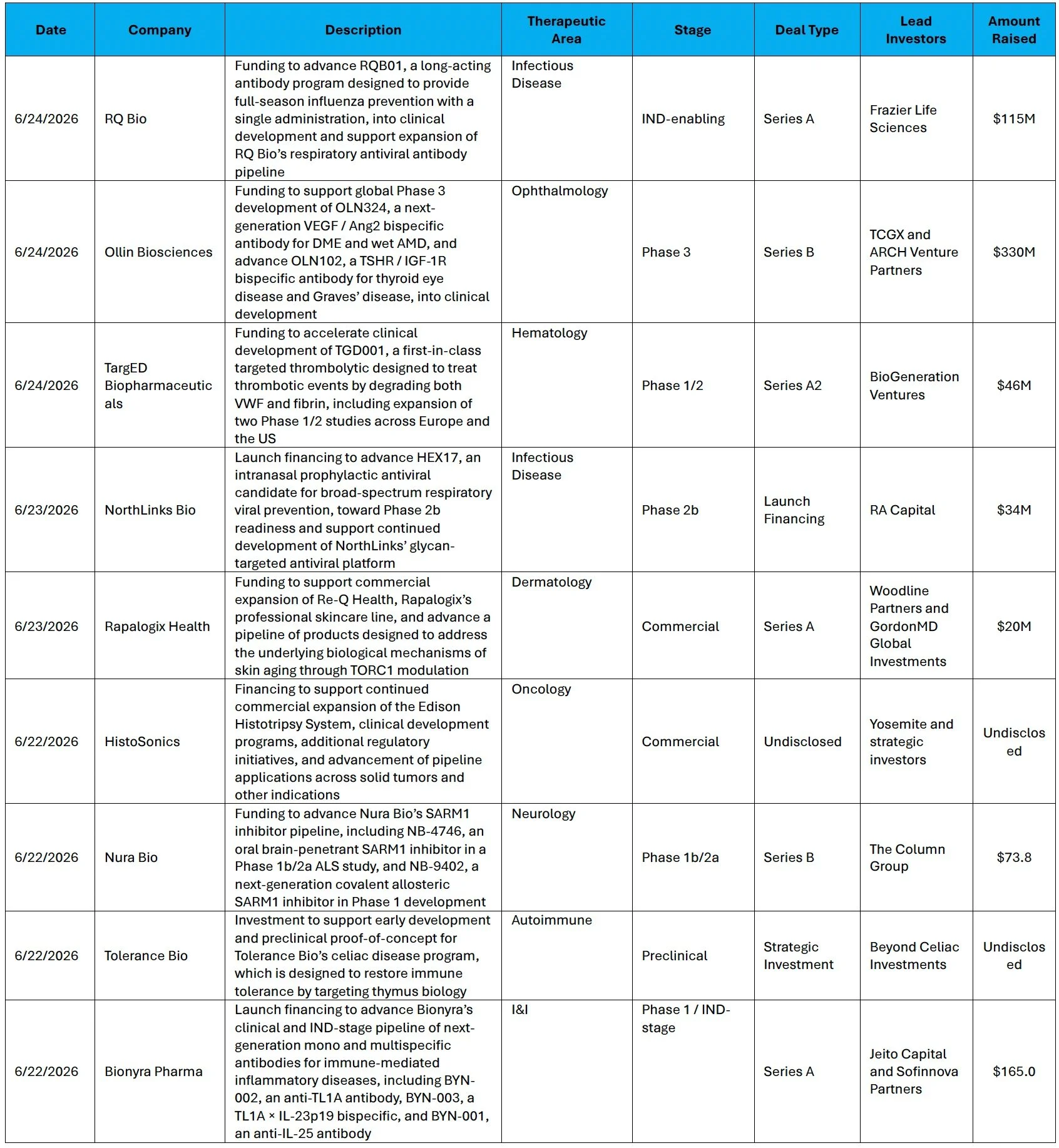

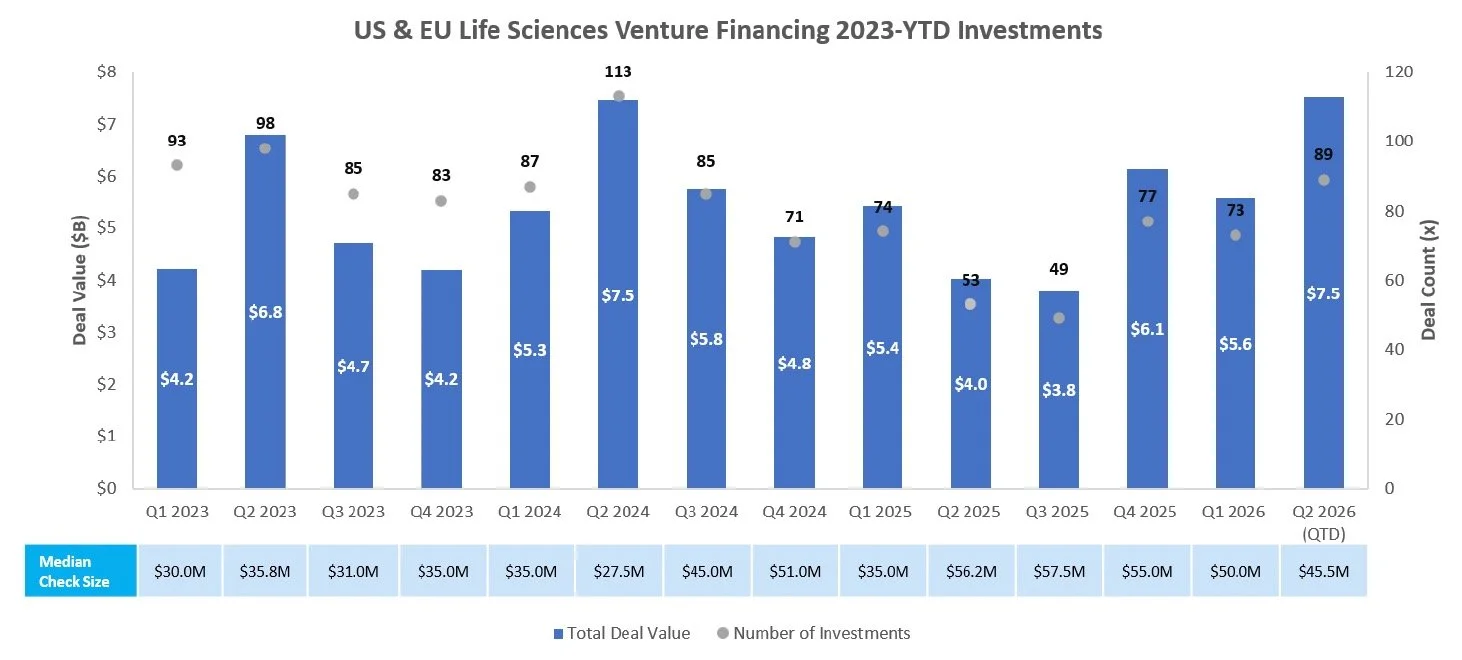

Venture Financing

VC investment focused on de-risked clinical opportunities, including late-stage ophthalmology through Ollin’s Phase 3 VEGF / Ang2 bispecific, immunology and inflammation biologics through Bionyra’s anti-TL1A and TL1A × IL-23p19 programs, and differentiated platforms across extracellular protein degradation and autoimmune T-cell engagers

Sources: Pitchbook, Biomedtracker, and CapIQ

A MAP to the Future of Targeted Oncology

The latest in our series of healthcare analyst reports focuses on the mitogen-activated protein kinase (MAPK) pathway, one of the most commonly perturbed signaling pathways in human cancer. Flowing from RAS to RAF to MEK to EKR, the pathway is a master regulator of cell growth and survival. Therefore, the amplification of proteins or mutation of key signaling domains are a common hallmark of cancer.

HEALTHCARE MARKET REPORTS ARCHIVE

-

-

-

April 17, 2026

April 24, 2026 -

-

-

-

-

-

-

-

-

-

-

-

-

-

-

CONNECT with the Authors >>

GREG BENNING

Partner, Managing Director, Head of Investment Banking

VASILIOS KOFITSAS

Partner, Managing Director, Investment Banking

JOHN ROGERS

Associate, Investment Banking

CRYSTAL HSU

Director, Investment Banking

ALEXA GILBERT

Analyst

About DNB Carnegie Back Bay

DNB Carnegie Back Bay drives global healthcare growth and innovation by providing a full range of strategic advisory and financing capabilities along the continuum of life science and healthcare company development. The DNB Carnegie Back Bay Healthcare Partnership is a marketing term referring to a strategic agreement between DNB Markets, Inc. and Back Bay Life Science Advisors. More information about the DNB Carnegie Back Bay Healthcare Partnership can be found here.

Securities products and services are offered in the US through DNB Carnegie, Inc., a US-registered broker-dealer and a separately incorporated subsidiary of DNB Bank ASA. DNB Carnegie, Inc. is a member of the Financial Industry Regulatory Authority (“FINRA”) and the Securities Investor Protection Corporation (“SIPC”). Securities products and services are offered in the European Economic Area through DNB Carnegie.