Week of July 17, 2026

The Week at a Glance:

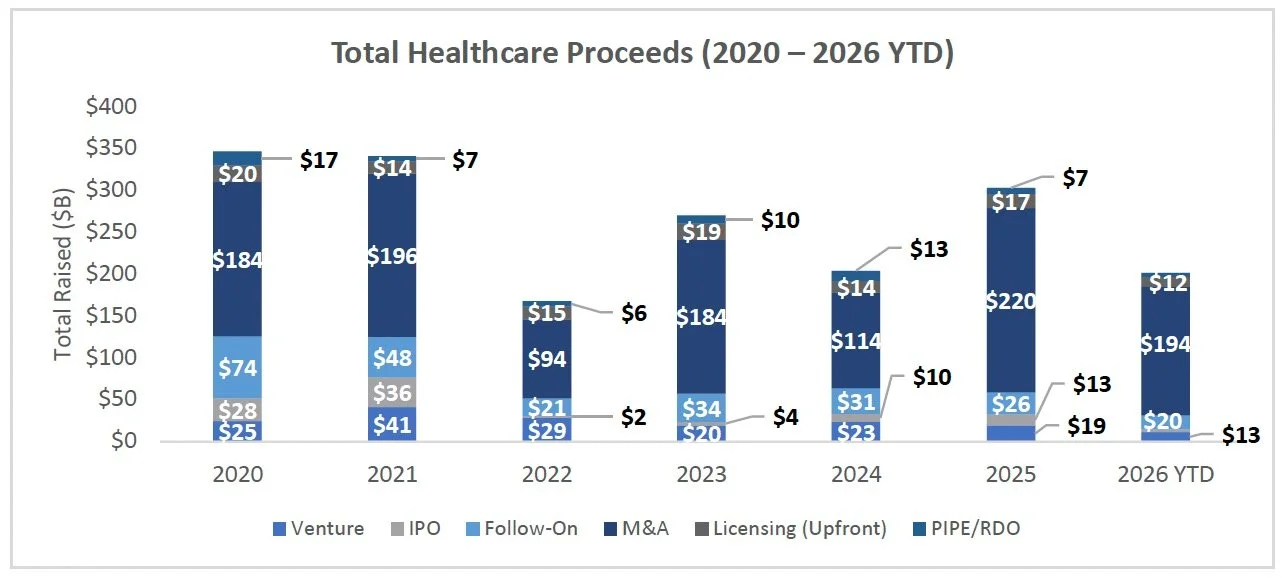

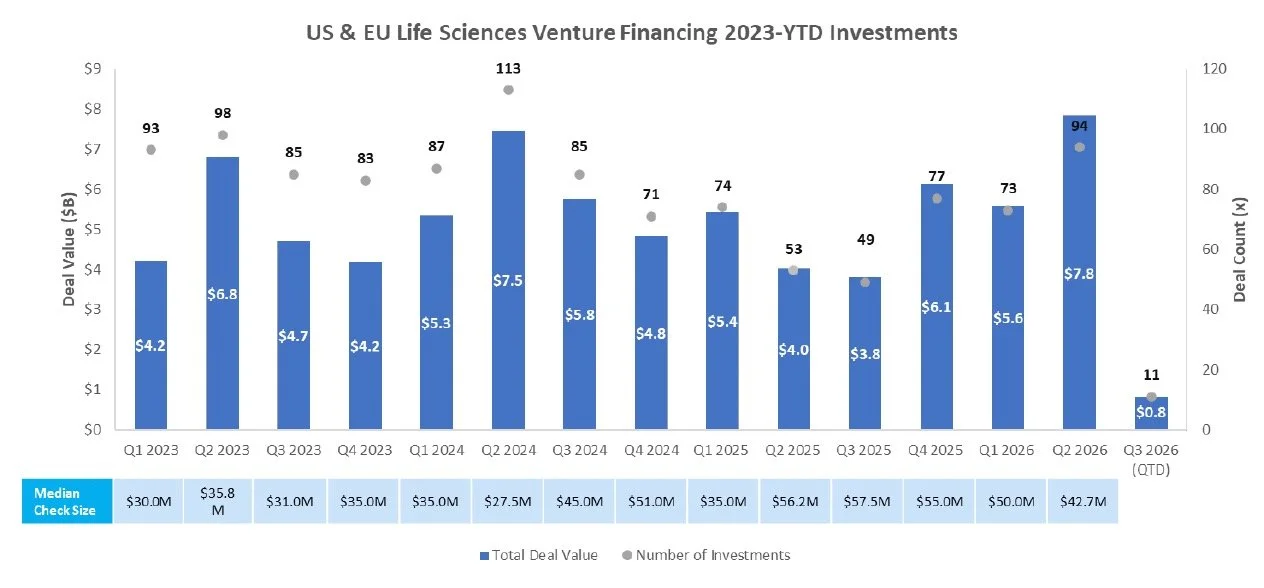

Healthcare Capital Markets Continue to Broaden: Six IPO filings, nearly $1B in follow-on activity, active PIPE issuance, and robust venture financing point to a continued reopening of healthcare capital markets across financing channels

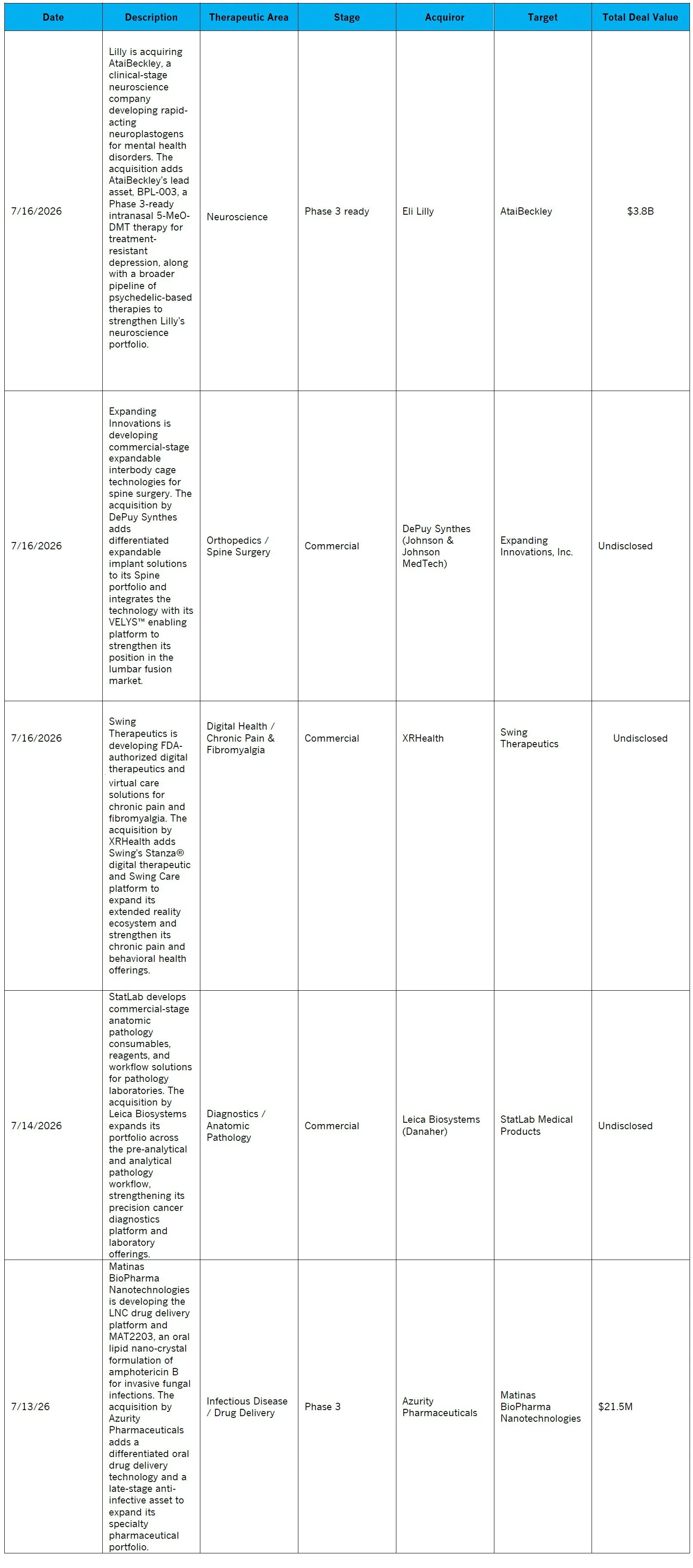

Lilly Doubles Down on Next-Generation Neuroscience: Lilly's $3.8B acquisition of AtaiBeckley marks another major investment in psychedelic therapeutics, signaling growing pharmaceutical confidence in novel CNS modalities

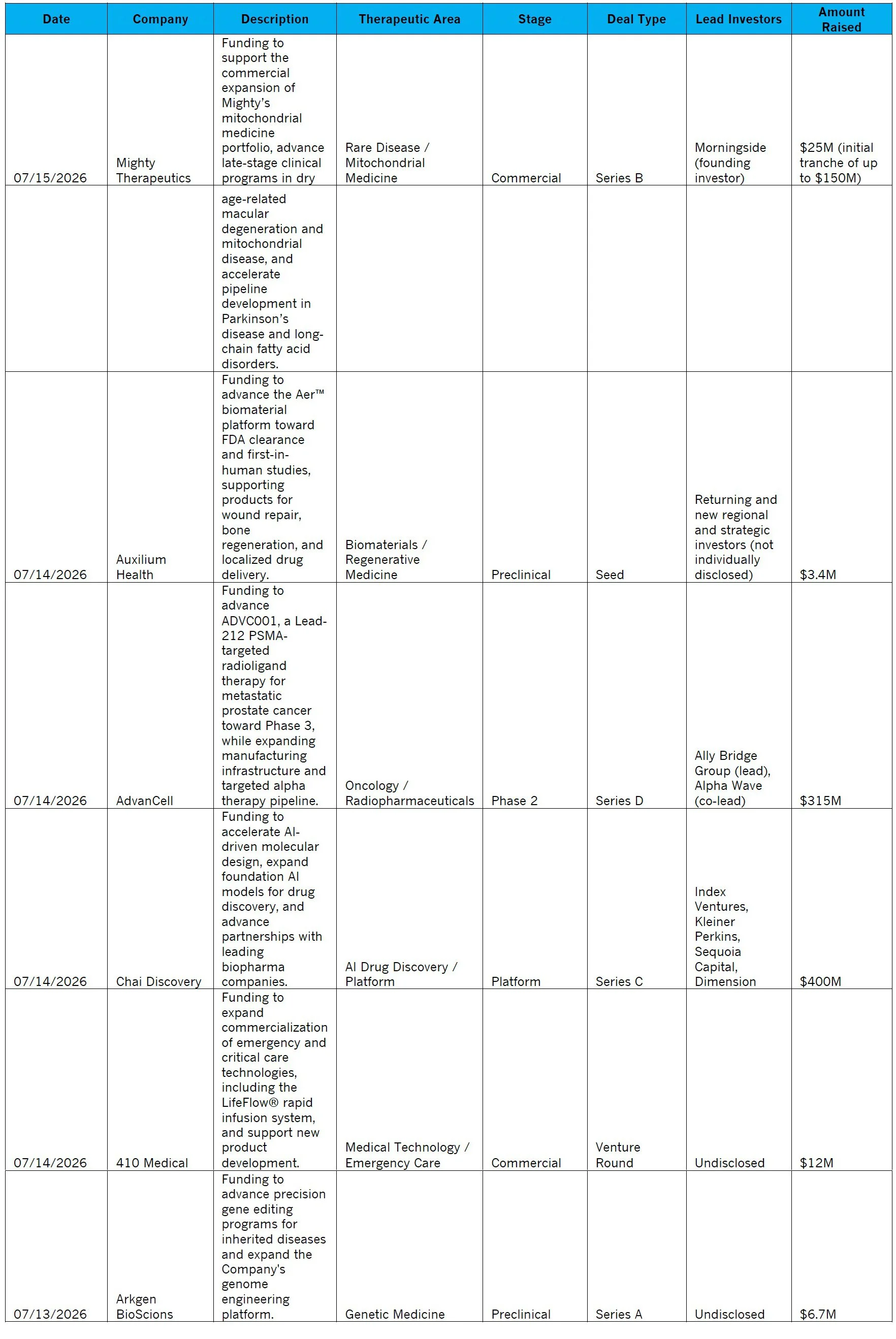

AI and Radiopharma Continue Attracting Capital: Large financings for Chai Discovery and AdvanCell reinforce continued investor interest for AI technologies within drug development and differentiated oncology innovation

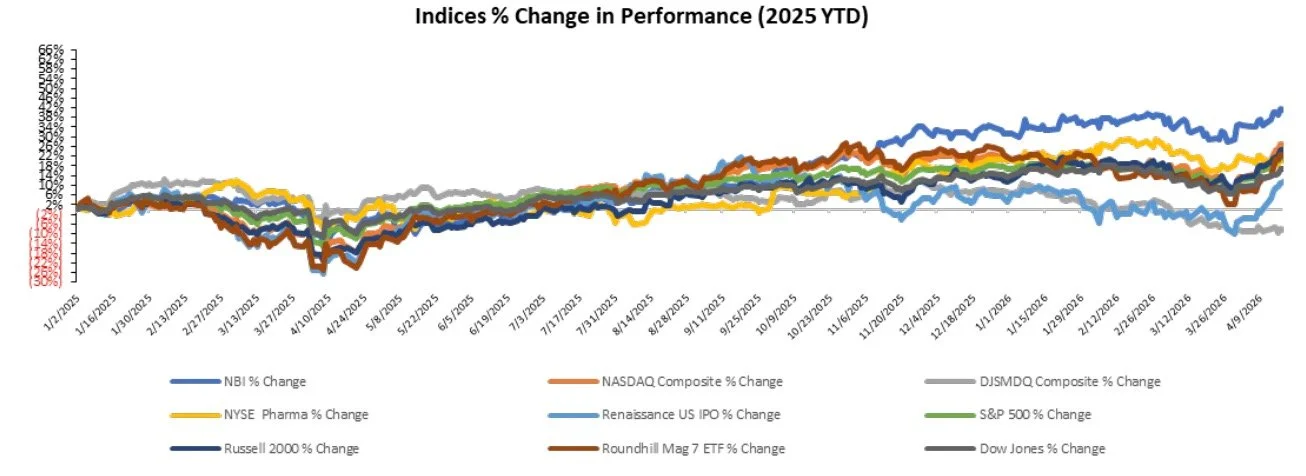

Markets Overview

Last week, healthcare outperformed the broader markets, as investors continue funding innovation

The S&P 500, Nasdaq, and Dow were down 0.8%, 1.4%, and 0.7%, respectively, last week

Markets pulled back slightly as investors prepare for Q2 earnings, with attention focused on growth forecasts as an indicator of broader underlying economic strength

The NYSE Pharma and NBI were up 0.3 and 0.5%, respectively, last week. Notable changes in share price included:

Q32 Bio (NASDAQ: QTTB): Shares rose 34.3% after the Company reported positive 36-week results from their Phase 2a trial evaluating bempikibart in patients with severe or very severe alopecia areata

Sources: Pitchbook, Biomedtracker, and CapIQ

Equity Markets

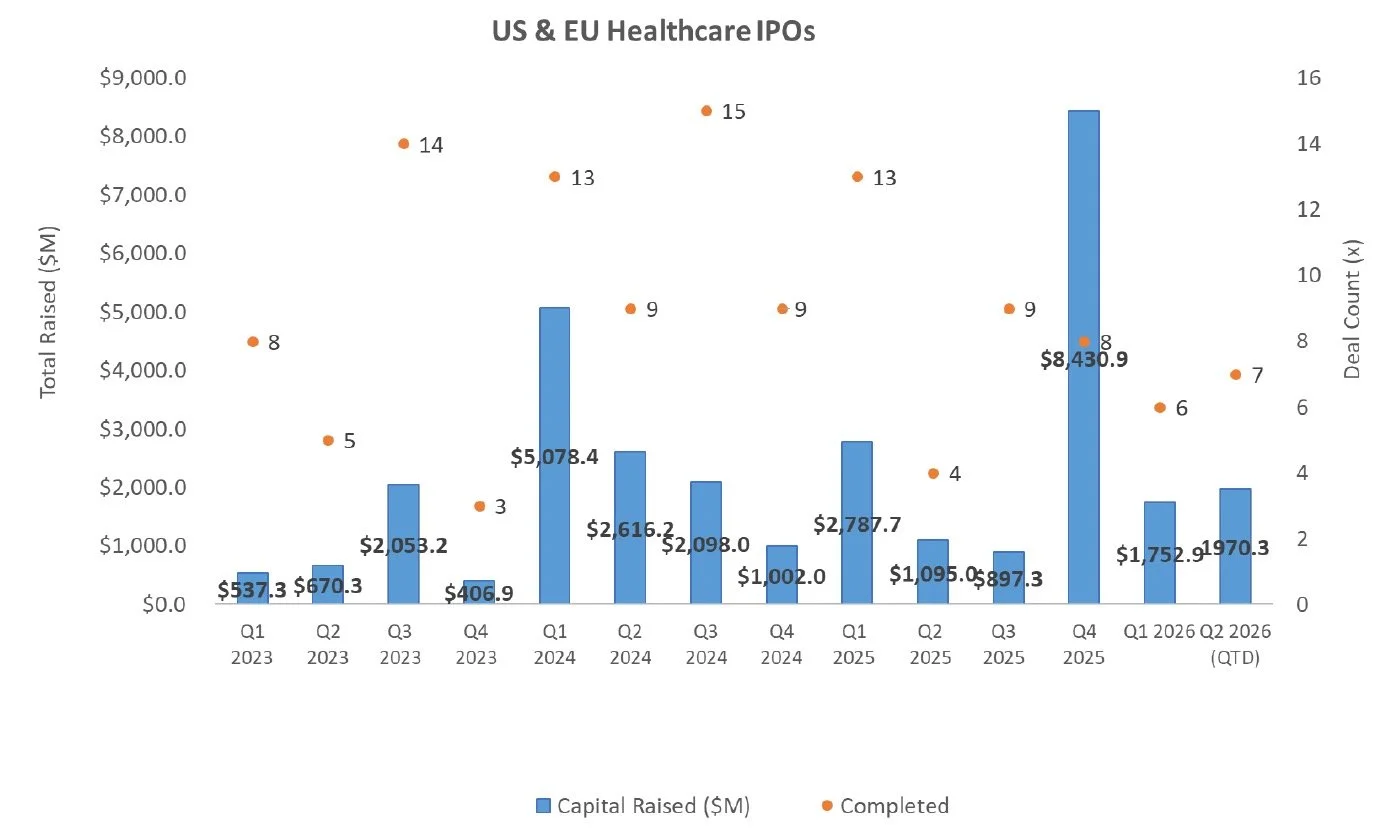

IPO

There were six S-1s filed last week, with the IPO pipeline continuing to expand across therapeutic areas

Attovia Therapeutics filed an S-1 for an IPO of up to $100M to advance its pipeline, led by ATTO-1310, a Phase 1b IL-31-targeting biologic being developed for chronic pruritus and high-itch atopic dermatitis, with Phase 2 initiation planned for the first half of 2027

Braveheart Bio filed an S-1 for an IPO of up to $100M to advance BHB-1893, a next-generation oral cardiac myosin inhibitor, into planned global Phase 3 trials in obstructive and non-obstructive hypertrophic cardiomyopathy

Vogenx filed an S-1 for an IPO expected to raise up to $75M to advance mizagliflozin, an oral, minimally absorbed SGLT1 inhibitor, including through the planned Phase 2b EMERGE trial in post-bariatric hypoglycemia

BlossomHill Therapeutics filed an S-1 for an IPO of up to $100M to advance BH-30643, a brain-active, mutant-selective OMNI-EGFR inhibitor currently in Phase 1/2 development, including into a planned potential registrational Phase 2 trial in C797S-positive EGFR-mutant NSCLC

Latigo Biotherapeutics filed an S-1 for an IPO of up to $100M to advance LTG-001, an oral NaV1.8 inhibitor, through planned Phase 3 bunionectomy and safety trials in moderate-to-severe acute pain, including postoperative pain

NuvOx Therapeutics filed an S-1 to raise approximately $20M to advance NanO2, an intravenous oxygen therapeutic in Phase 2b studies for glioblastoma and acute ischemic stroke, while also supporting ARDS development and preparations for a pivotal Phase 3 glioblastoma trial

IPOs priced in 2025 and 2026 have generated a median and average return of 24.1% and 32.3% YTD, respectively:

After-Market Performance by Stage

Clinical-stage after-market performance: 48.7% (average), 13.8% (median)

Commercial-stage after-market performance: 15.3% (average), 25.8% (median)

After-Market Performance by Sector

Biopharma: 48.7% (average), 13.8% (median)

MedTech: 10.8% (average), 13.2% (median)

Source: CapIQ

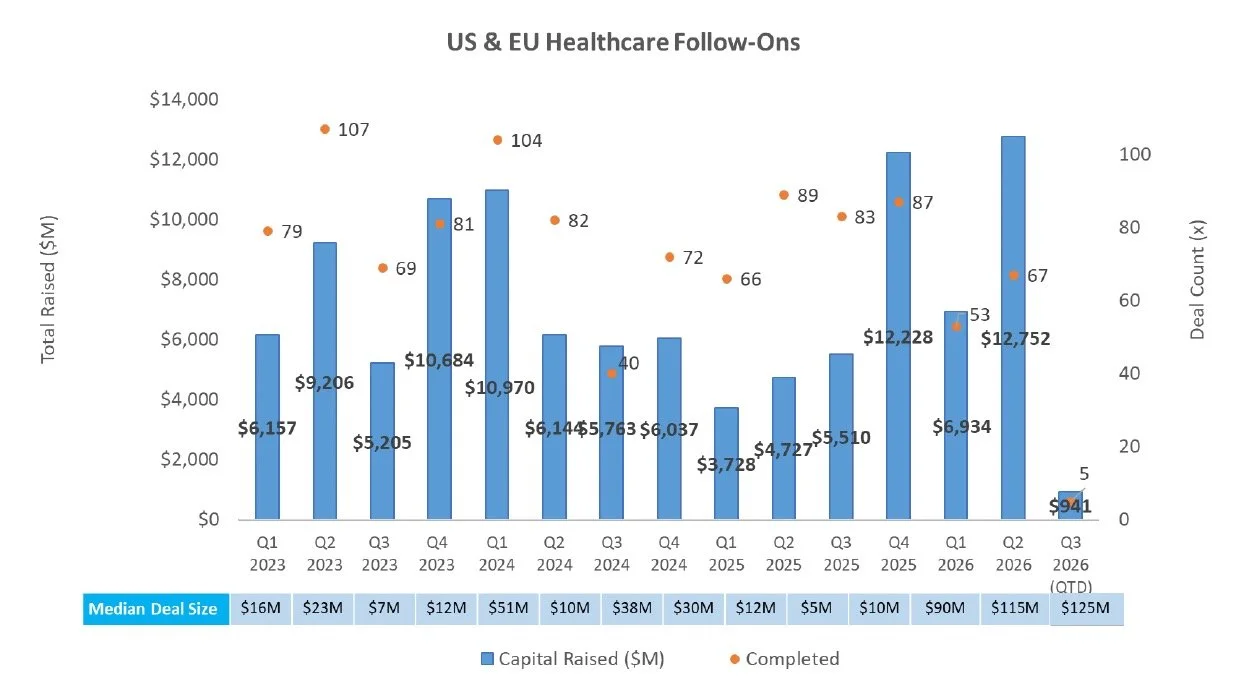

Follow On

Follow-on activity was led by Erasca as investors continue to focus on the RAS class within PDAC following Revolution Medicines’ unprecedented data in the indication

There were four follow-on equity offerings totaling approximately $937M this week

Crescent Biopharma (NASDAQ: CBIO) closed a $143.7M upsized public offering, including the full exercise of the underwriters' option to purchase additional shares, to advance its clinical-stage oncology pipeline, including CR-001, a PD-1 × VEGF bispecific antibody, and its antibody-drug conjugate (ADC) programs for the treatment of solid tumors

Q32 Bio (NASDAQ: QTTB) closed a $200M public offering of common stock and pre-funded warrants to support the continued clinical development of bempikibart for alopecia areata and other autoimmune and inflammatory diseases, as well as research, commercialization activities, working capital, and general corporate purposes

Erasca (NASDAQ: ERAS) closed a $550M upsized public offering to advance its clinical-stage precision oncology pipeline targeting RAS/MAPK pathway-driven cancers, including ERAS-0015 and other RAS-targeted programs, as well as fund research and development, working capital, and general corporate purposes

Source: Biomedtracker

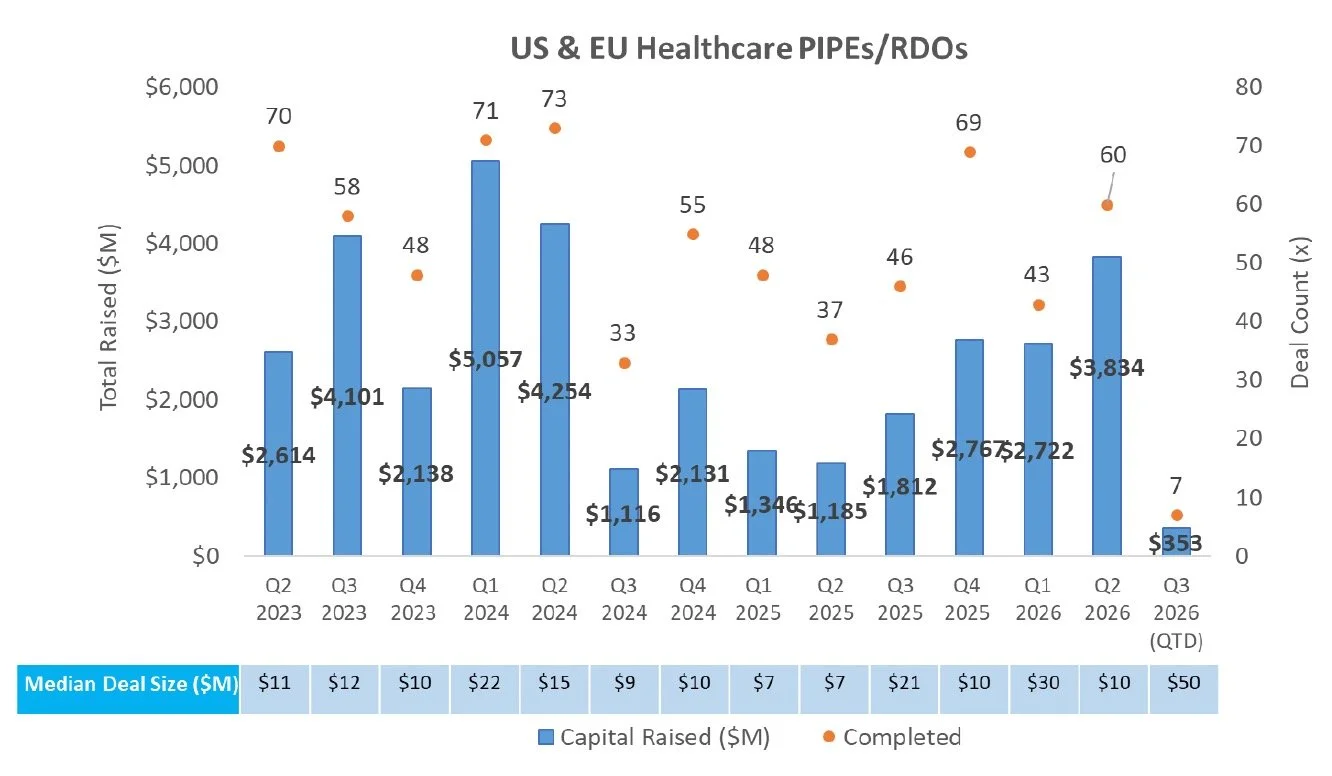

PIPE/RDO Markets:

PIPE / RDO activity was concentrated in Alto Neuroscience, a clinical-stage biotech developing therapies for psychiatric disorders, amid growing strategic and investor interest in the space

There were three PIPEs / RDOs announced last week, representing aggregate proceeds of $195M. Of note:

Alto Neuroscience raised $100M through an underwritten registered direct offering led by BofA Securities, Stifel, William Blair, and Baird, with newly issued common shares priced at $26.48 apiece, with proceeds expected to accelerate and expand clinical development of ALTO-207, including an additional planned Phase 3 trial as monotherapy for the treatment of treatment-resistant depression, and for general working capital

o Agenus raised $85M through a private placement led by Commodore Capital, with participation from RA Capital Management, TCGX, Invus, and Ligand Pharmaceuticals, with common shares priced at $3.69 apiece, with proceeds expected to fund ROBBIN, its registrational Phase 3 trial of neoadjuvant botensilimab and balstilimab (BOT+BAL) in microsatellite-stable (MSS) colon cancer

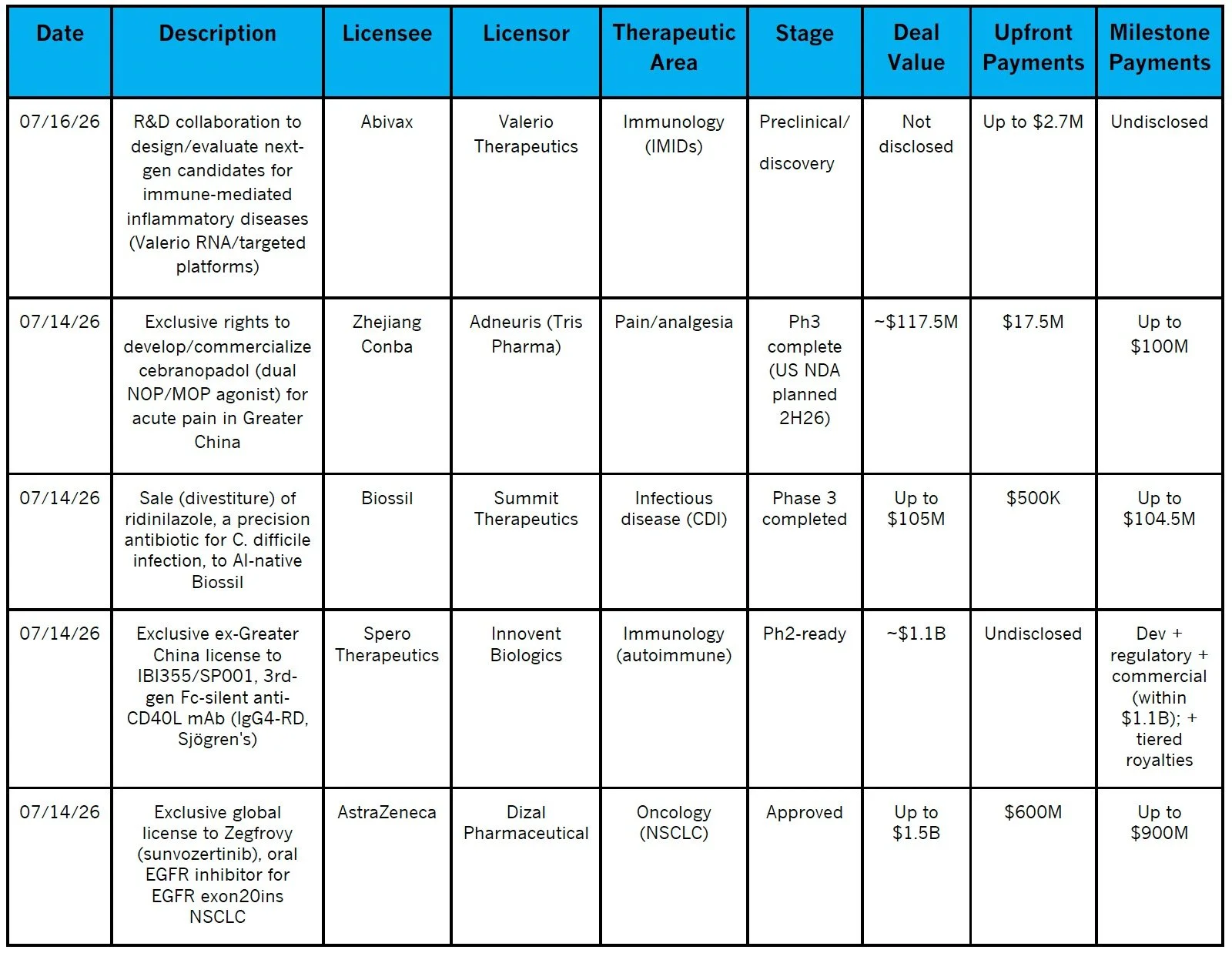

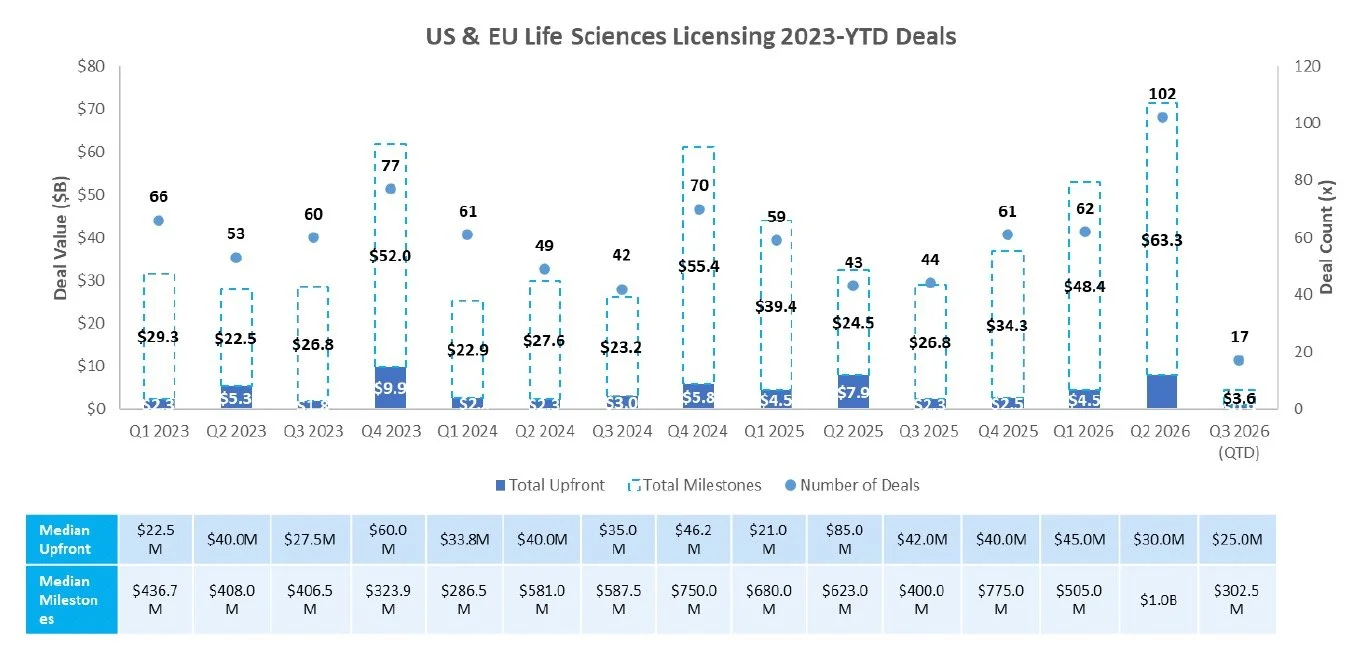

Licensing

Immunology and oncology led licensing activity, with value concentrated in Phase 3 and approved assets

AstraZeneca’s licensing deal for Dizal’s EGFR inhibitor sunvozertinib increases competitive pressure on ArriVent and Taiho/Cullinan in EGFR exon 20 insertion–positive NSCLC

Sources: Pitchbook, Biomedtracker, and CapIQ

Sources: Pitchbook, Biomedtracker, and CapIQ

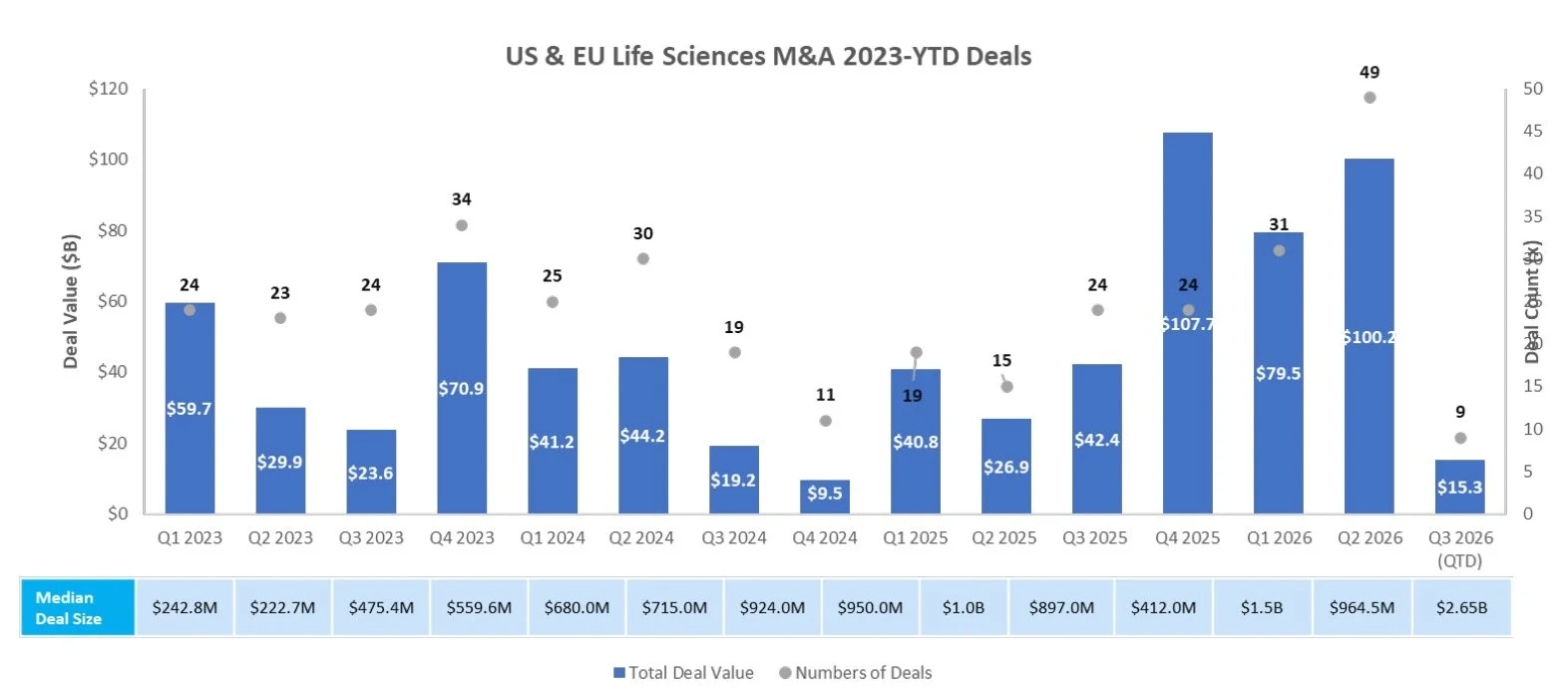

M&A

Eli Lilly’s acquisition of AtaiBeckley marks the year’s second sizable psychedelics transaction, though the modest 26% premium may suggest either that the company was fairly valued at its previous trading levels or that competitive tension in the transaction process was limited

Venture Financing

VC investment focused on AI-enabled platform technologies and differentiated therapeutic platforms, with large financings supporting Chai Discovery's molecular design platform and AdvanCell's targeted alpha therapies

Sources: Pitchbook, Biomedtracker, and CapIQ

A MAP to the Future of Targeted Oncology

The latest in our series of healthcare analyst reports focuses on the mitogen-activated protein kinase (MAPK) pathway, one of the most commonly perturbed signaling pathways in human cancer. Flowing from RAS to RAF to MEK to EKR, the pathway is a master regulator of cell growth and survival. Therefore, the amplification of proteins or mutation of key signaling domains are a common hallmark of cancer.

HEALTHCARE MARKET REPORTS ARCHIVE

-

-

-

-

April 17, 2026

April 24, 2026 -

-

-

-

-

-

-

-

-

-

-

-

-

-

-

CONNECT with the Authors >>

GREG BENNING

Partner, Managing Director, Head of Investment Banking

VASILIOS KOFITSAS

Partner, Managing Director, Investment Banking

JOHN ROGERS

Associate, Investment Banking

CRYSTAL HSU

Director, Investment Banking

ALEXA GILBERT

Analyst

About DNB Carnegie Back Bay

DNB Carnegie Back Bay drives global healthcare growth and innovation by providing a full range of strategic advisory and financing capabilities along the continuum of life science and healthcare company development. The DNB Carnegie Back Bay Healthcare Partnership is a marketing term referring to a strategic agreement between DNB Markets, Inc. and Back Bay Life Science Advisors. More information about the DNB Carnegie Back Bay Healthcare Partnership can be found here.

Securities products and services are offered in the US through DNB Carnegie, Inc., a US-registered broker-dealer and a separately incorporated subsidiary of DNB Bank ASA. DNB Carnegie, Inc. is a member of the Financial Industry Regulatory Authority (“FINRA”) and the Securities Investor Protection Corporation (“SIPC”). Securities products and services are offered in the European Economic Area through DNB Carnegie.